{kind=link}

Picture supply: Getty Photographs

Warren Buffett’s funding method entails specializing in blue-chip corporations with a nasty popularity. With shares nearing all-time highs, I am considering of doing the identical.

Simply over a decade in the past, his funding car was Berkshire Hathawaypurchased a big stake in an agricultural tools firm. john deere amidst the agricultural recession. And my newest concepts are alongside these strains.

Buffett’s funding

From 2012 to 2016, Berkshire bought simply over 7% of Deere’s excellent inventory. This was a time when low agricultural costs had been weighing on the business.

In some ways, this was a traditional Buffett funding. Shares of blue-chip corporations commerce at a reduction on account of momentary issues. Nonetheless, issues did not go fully to plan. Crop costs took a very long time to get better and had been in a protracted downward cycle till round 2020. And that was lengthy sufficient for Berkshire to desert the funding.

This reveals that even with the perfect corporations within the business, there isn’t a assure that your funding will work out. However I am at the moment contemplating comparable concepts for my portfolio as nicely.

long run progress

The shares I am being attentive to are CNH Industrial (NYSE:CNH). Like Deere in 2012, the corporate is a farm tools maker that’s buying and selling at reductions on account of falling crop costs.

This concept did not work ten years in the past. Nonetheless, I believe the rise of automation in agriculture implies that investing now is not only about ready for the financial cycle to get better.

It’s a lot simpler to construct a self-driving tractor than a self-driving automotive if there isn’t a site visitors round. CNH goals for this enterprise to account for 10% of gross sales by 2030.

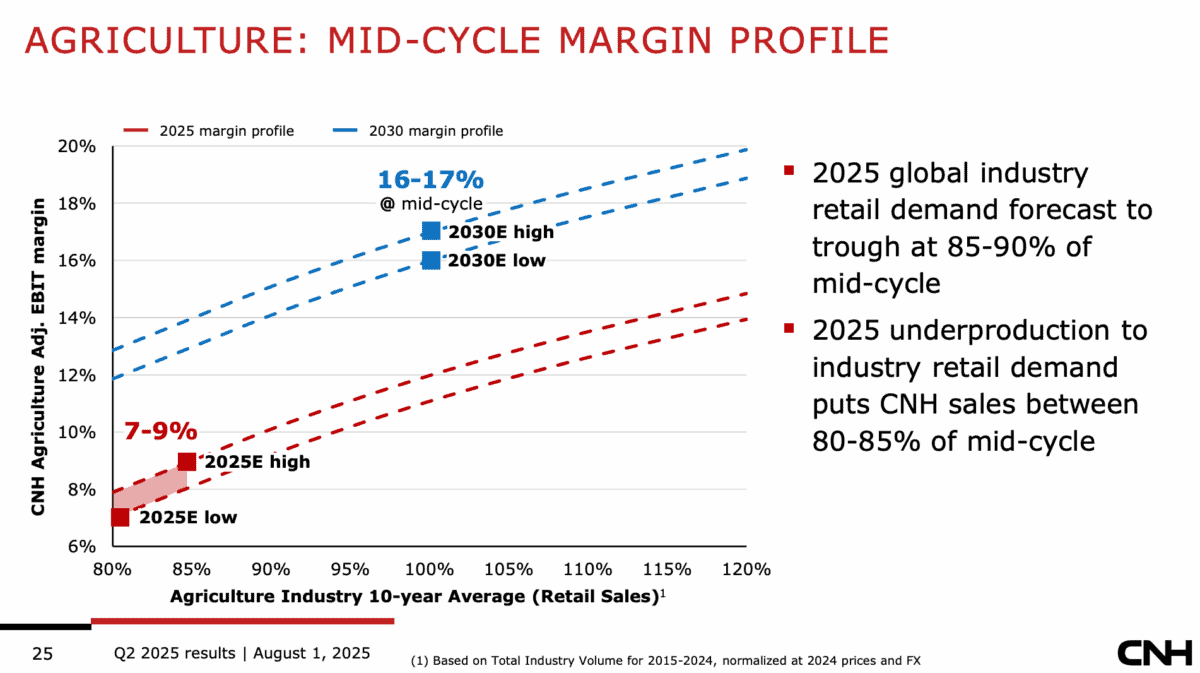

Supply: CNH Q2 Outcomes Presentation

That is double the present stage, and the corporate expects this to imply its agricultural enterprise’s margins will improve from round 8% to 16%. Different issues being equal, it means the revenue is doubled.

unfavorable analysis

The corporate’s inventory trades at a ahead worth/earnings ratio (PER) of roughly 14 occasions. That is considerably decrease than the price-to-earnings ratio (PER). S&P500 It’s a median worth and relies on diminished revenues on account of decrease crop costs.

The corporate has a considerable amount of debt on its stability sheet, which poses dangers, particularly if rates of interest do not fall as anticipated. Nonetheless, this isn’t at all times so simple as it appears.

Roughly 80% of the corporate’s debt is financed by mortgage receivables. In different phrases, that is the money that companies lend and borrow to finance buyer purchases.

I do not assume CNH’s debt shall be a problem if its clients adjust to their money owed. If not, the tools used as collateral could be seized to offset losses.

discover shares to purchase

In a 2022 interview, Berkshire investor Todd Combs outlined three issues Buffett appears to be like for in shares he buys. And I believe CNH can meet all of them.

The primary is that the ahead P/E ratio is lower than 15. Second, there’s a 90% probability that earnings will develop over 5 years, and third, there’s a 50% probability that earnings will develop at a price of seven% per 12 months.

The rise of automation within the agriculture business ought to result in sustained progress. And we need to make the most of the unusually low ranges of agricultural produce.