{kind=link}

Picture Supply: Getty Photographs

FTSE 100I have been an enormous delay for a very long time S&P 500. Over the previous decade, US indexes have been fueled by a surge in tech valuations, leaving the UK flagship index caught beneath the burden of lifeless banks and oil giants.

Nevertheless, 2025 introduced surprises. Up to now, footsea has returned to over 7%. That is a dramatic change in comparison with latest years, and an indication that the UK’s blue chips are lastly holding their very own.

Please dig just a little deeper. It is clear what that is transferring. A small variety of FTSE shares have overwhelmed expectations and outperform virtually all main US corporations.

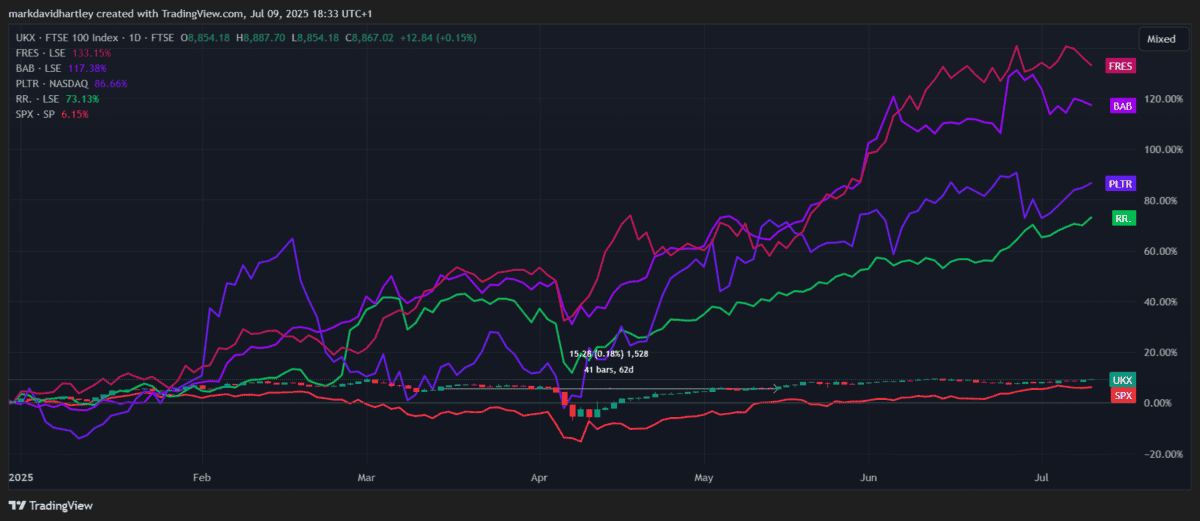

Silver Minor targeted on Mexico Fresniro Engineering heavyweight has elevated by over 130% Babcock‘s soared 116% Rolls-Royce It went on to run for an astonishing multi-year interval, incomes a further 73% in 2025 alone.

Just for all S&P 500 corporations, PalantirHe was within the prime three, barely outstriking the roll at 84% this yr. It is fifth place NRG Powera rise of 65% per yr.

What’s the surge in?

A lot of the expansion comes right down to a particular tailwind. Valuable metals are rising amid international uncertainty and fueling Fresniro. The protection finances is booming, supporting Babcock and Roll. In the meantime, the recovered oil costs and resilient international demand have helped many FTSE stubborns.

However a few of these strikes could also be forward of themselves. Inventory costs which can be rocketing on hope alone can simply turn into “development traps.” Right here, evaluation is separated from the long-term foundation. That is why I wish to keep an affordable outlook when the market will get just a little loopy.

There are sometimes extra sturdy income, cheap valuations and stable stability sheets in the long term than short-term worth will increase.

Extra cautious FTSE 100 picks

There’s one inventory that’s now appearing extra “rationally” Beadley (LSE:BEZ). Specialised insurance coverage corporations have skilled quiet, average development this yr, up 8.8%. There’s nothing flashy, but it surely’s snug forward of the historic common of the index.

Extra importantly, it’s supported by stable behavioral tendencies. Earnings per share elevated 9.9% year-on-year, whereas income elevated 7.8%. It’s powered by a sound internet revenue of 18% and a formidable 26.3% inventory return ratio (ROE).

The opinions additionally look enticing. The inventory is buying and selling at a worth of simply 6.67 (P/E) ratio and a a number of of 1.55 (P/B), suggesting that traders usually are not paying this high quality development potential.

It is not a giant revenue play, however the dividend yield of two.8% is nicely lined by a cost fee of simply 18.3%. Free money circulate is at £1.26 billion and is snug exceeding its £614 million debt. Moreover, dividends have been operating for 3 years.

The dangers of seeing

After all, insurance coverage can turn into a risky enterprise. Beazley is uncovered to huge losses associated to huge astastrophe and will curb income in sure years. They’re additionally weak to the pricing cycle of specialised insurance coverage. This lets you swing rapidly from the worthwhile ones as competitors turns into extra intense.

However total, I believe it is type of stable UK enterprise that it is value contemplating sturdy reliability.

Development inventory fluctuates wildly, however these secure compares are traded with sensible valuations, typically resulting in the best returns over time. When constructing a various long-term portfolio, that is precisely what traders must be on the lookout for.