{kind=link}

Picture supply: Getty Pictures

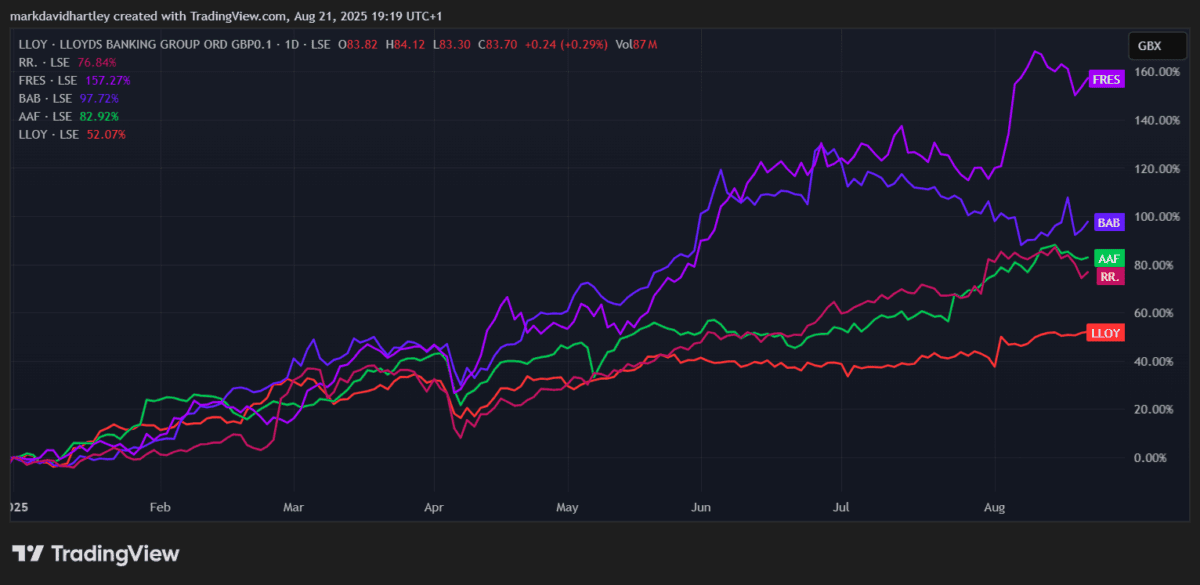

Roy’s‘(LSE:LLOY) shares continued to climb seemingly endlessly this week, growing their year-long complete earnings to an astonishing 54%.

Only a handful FTSE 100 The shares are getting higher Fresniro, Babcock, Airtel Africa And it is well-liked Rolls-Royce. Throughout the financial institution, Lloyds leads the pack. Nut waist and Barclays It is up about 40% Normal Constitution It rose 37% HSBC twenty 4%.

It is a turnaround for banks that had been broadly seen as serial underperformers a very long time in the past.

Rushing practice?

RBC Capital Market just lately introduced that it has introduced a European financial institution.Pace practice” in analysis notes. Whereas that sounds thrilling, analysts additionally highlighted how susceptible the sector is to geopolitical and macroeconomic shocks. German banks and OSB Group.

Goldman Sachs It additionally takes a extra bullish angle, elevating its value goal for Lloyds’ inventory from 87p to 99p earlier this month. On common, 18 analysts have a look at shares heading in direction of 90.7 factors than the next 12 months. It is about 8% dearer than as we speak. Eleven analysts have robust purchase rankings, whereas eight are caught on maintain.

It looks as if my confidence is getting again vastly.

Paypoint Partnership

One other promising improvement is information of Lloyds’ partnership Paypoints. By way of BankLocal Providers, Group clients will quickly be capable to create money deposits at over 30,000 places throughout the UK.

This implies easy and handy entry to pay as much as 300 kilos a day with notes and cash, and inside minutes your cash will seem in your account. Importantly, Lloyds is to develop into the primary Excessive Avenue Financial institution to completely embrace this scheme.

In an age the place financial institution branches are closing at a record-breaking tempo, it seems to be like a clever transfer that may assist maintain clients loyalty.

Dependable earnings…for now

Revenue stays an necessary cause why many traders purchase Lloyds shares. Nonetheless, the current rally has pushed dividend yields to beneath 4% for the primary time in almost three years.

Nonetheless, dividends are growing. The forecast means that funds may attain 4.7p per share by 2027. This is a rise of 48% from as we speak’s 3.17p. Historical past exhibits that warning is required, however not unhealthy in any respect. When Covid hit, Lloyds lower its dividend in half. If an identical shock recurs, shareholders may face the identical disappointment.

Rates of interest and inflation stay threat elements. Any sudden change may hit the profitability of the financial institution.

Nonetheless worth?

All this progress will not be seen. Lloyds’ ahead value income (P/E) ratio is at 11, larger than NatWest, HSBC and Barclays. Its debt-to-fair ratio is especially larger than most friends.

That means that Lloyds may now not be the discount they as soon as had been. However whereas the perfect earnings might already be in your bag, you would not anticipate the expansion story to vanish in a single night time.

For long-term earnings traders, Lloyds continues to contemplate the engaging FTSE 100 choose. The rankings are now not low cost, however dividends are set to rise, and there are nonetheless robust instances of possession of this UK financial institution big, with new providers just like the Paypoint Partnership growing their worth.