{kind=link}

Picture supply: Getty Photographs

tesco (LSE:TSCO) inventory rose simply 1% on Wednesday, April eighth. in the meantime, marks and spencer It rose almost 7%.

So what is going on on? Let’s discover.

by no means received hit

When the battle began within the Gulf, the market fell. But it surely wasn’t even. In actual fact, some shares, comparable to oil and transport, rose.

Tesco wasn’t a gainer, however traders had been gradual to promote their shares. FTSE100 grocery retailer. And it is all about threat.

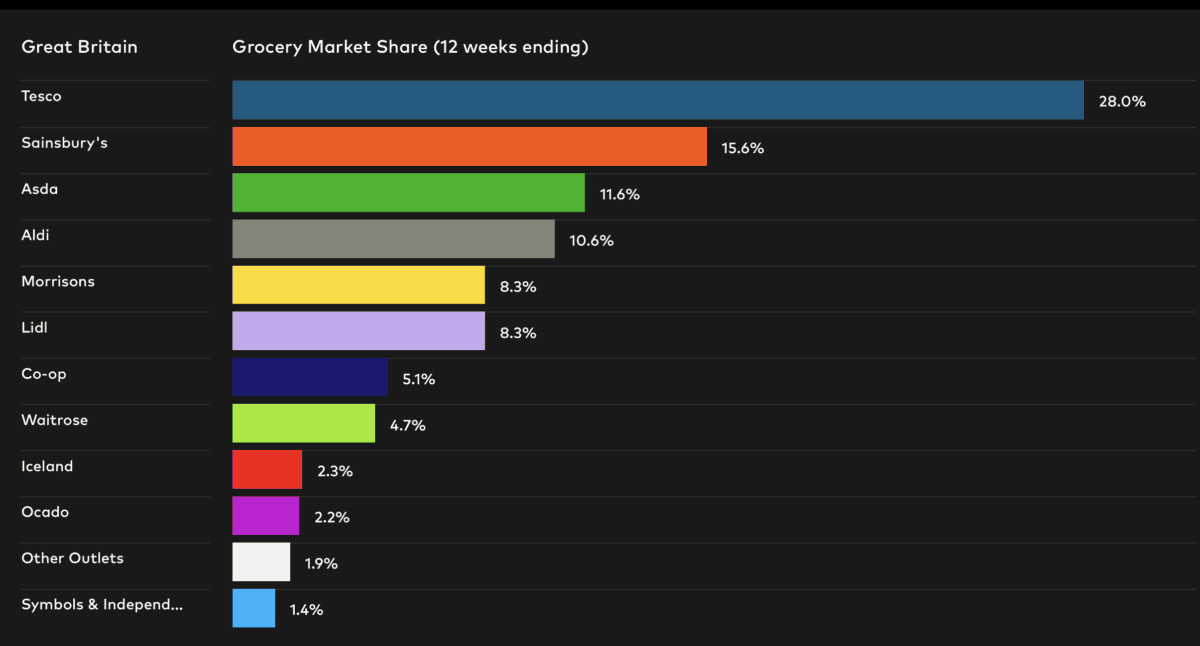

Tesco sells groceries. Individuals purchased them earlier than and through the conflict, and they’ll proceed to purchase them now. Due to their predictability, fund managers name them defensive shares, or shares which are much less delicate to enterprise cycles. When the world turns into unsure, cash tends to move into shares like Tesco, relatively than away from them. Not thrilling, however dependable.

That dynamic protected Tesco when it was down. The identical dynamics work in opposition to it right this moment. The ceasefire was a risk-on occasion, with traders returning cash to the banks, airways and residential builders that had the largest sell-offs. Tesco wasn’t offered exhausting, so there will not be a tough rebound. You may’t regain floor you have by no means misplaced.

In actual fact, there are a number of extra nuances right here. Tesco is extra cost-efficient than its friends, and if value inflation continues, clients could commerce down from Marks & Spencer to friends like Tesco.

However there is no doubt that rising oil and power costs are hurting the grocery store giants. Logistics automobiles, deliveries, and fridges are in operation.

Transactions very near truthful worth

Tesco is the UK champion. It’s an operational masterpiece, and its model energy is sort of unparalleled. It has additionally confirmed its skill to face as much as competitors from friends comparable to Lidl and Aldi. As such, it deserves to commerce at some premium to its friends.

It additionally gives extremely secure efficiency. Revenues have elevated yearly because the pandemic and are anticipated to extend equally in 2026 and 2027.

The tough half, nevertheless, is figuring out how massive that premium ought to be. Tesco presently trades at round 15.3 occasions anticipated earnings, has a dividend yield of three.3% (coated by earnings 1.99 occasions) and has web debt of £10.3 billion (round 11 occasions web earnings).

On the different finish of the dimensions is Marks & Spencer. The corporate’s anticipated earnings are 10.3 occasions, the dividend yield is 1.96% (5.04 occasions coated by earnings), and the corporate has web debt of £2.5 billion (about 6 occasions web revenue).

my view

Tesco is a superb firm. Nevertheless, I am beginning to assume that this premium is a bit unreasonable. Institutional analysts agree that the inventory is presently buying and selling at simply 1% above its value. It might nonetheless be value contemplating, however I am certain there are different issues on the market which are extra worthwhile.