{kind=link}

Picture supply: Getty Photographs

When on the lookout for progress shares to purchase, the UK will not be your high precedence. In spite of everything, the next tech inventory riots: Nvidia and Palantir It’s written on the opposite aspect of the pond. That is a rise of 627% and 1,665%, respectively, in simply three years.

Nevertheless, there are some robust progress corporations within the UK which can be lesser identified. At present I would like to spotlight two that I believe are price a more in-depth look.

smart

Let’s begin with the largest one, smart (LSE: Smart). The worldwide cash switch specialist has a market capitalization of £10.8bn. FTSE100the primary itemizing location might be moved to the US.

Nevertheless, it plans to take care of its secondary itemizing in London, which is at present priced at 1,050 pence per share. Consequently, the anticipated value/earnings ratio (PER) of the corporate’s inventory is 26.5 occasions.

I do not suppose that is outrageous for an organization that did the next final yr:

- Underlying revenue elevated by 19% at fixed forex to £1,619m.

- Cross-border buying and selling quantity elevated by 25% to £181.7bn.

- The variety of prospects elevated by 21% to 18.9 million.

- Pre-tax revenue margin is anticipated to achieve 16%.

Trying to the long run, it appears to me that the expansion engine stays very robust. Along with individuals, extra companies are signing up to make use of Smart, and its infrastructure has made cross-border transactions cheaper and quicker. Presently, roughly 75% of remittances are made immediately.

Moreover, Smart is reducing its take price because it scales up. Whereas some buyers might not like this as a result of it sacrifices short-term profitability, it ought to put Smart in a stronger aggressive place in the long run.

And as a long-term investor, that is what pursuits me.

Nevertheless, within the quick time period, the state of affairs within the Center East poses a danger to progress. If the worldwide economic system had been to fall right into a droop as a result of inflation and rising power prices, fewer individuals and companies would have the ability to transfer cash round.

Regardless of this danger, I am pleased to have Smart in my high 10 portfolio. The share value is up 21.5% because the starting of the yr, however I believe it is nonetheless price contemplating at round £10.

Me

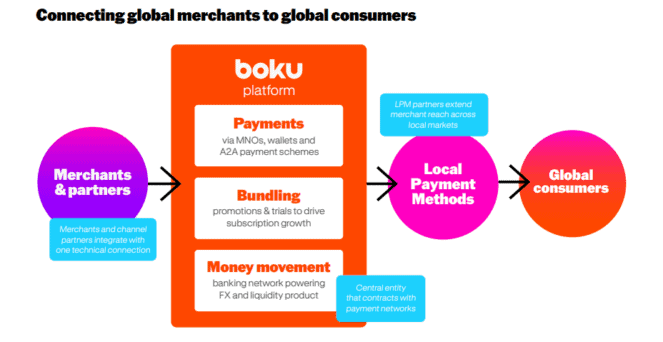

flip to Me (LSE:BOKU) That is now a a lot smaller firm, with a market capitalization of £525m. Though we’re not that large, Boku works with among the world’s largest retailers, serving to them promote gross sales in additional than 60 international locations by native cost strategies (LPMs).

For instance, for example somebody in Thailand desires to subscribe. Netflix. They select a digital pockets as their cost methodology and I present the backend pipe that connects Netflix with their particular native pockets. Its community at present stands at over 200 LPMs and is rising yearly.

Income final yr reached £129m, up 30% from £62m in 2021. Analysts anticipate its income to achieve greater than £210m by 2028, with LPM anticipated to account for 60% of the $11tn world e-commerce market.

Nevertheless, we’re not a loss-making fintech firm. The corporate’s income have been rising together with important gross sales enlargement, and administration is assured that revenue margins will enhance sooner or later.

The excellent news is that this earnings progress would not look like priced in, with the inventory buying and selling at simply 18 occasions subsequent yr’s anticipated earnings. That is low cost for a scalable platform that’s anticipated to proceed rising at 20% over the medium time period.

Once more, a downturn within the world economic system can also be a danger, as is competitors within the funds house. Nevertheless, I believe this under-the-radar inventory is price contemplating for the subsequent 5 years.