{kind=link}

Picture supply: Getty Pictures

After rising almost 500% in 10 years. gregs” (LSE:GRG) share worth started to fall in direction of the top of 2024. This coincided with the federal government’s new enterprise tax enhance plans.

Greggs’ share worth has plunged 42% since October 2024, when Chancellor of the Exchequer Rachel Reeves introduced an increase in Employer Nationwide Insurance coverage and lowered the edge. This makes your £5,000 funding value £2,900, excluding dividends.

Not solely did the finances enhance Mr Greggs’s employees prices, nevertheless it additionally undoubtedly had a chilling impact on the UK economic system. Many corporations have suspended hiring and unemployment has risen, with the unemployment price now at a five-year excessive.

In 2023, Greggs’ whole gross sales and like-for-like gross sales (LFL) grew by 19.6% and 13.7%, respectively. In 2025, these figures have been 6.8% and a pair of.4%, with underlying working revenue down 4% to £188m.

Greggs below strain

Within the first 9 weeks of 2026, LFL development slowed additional to 1.6%. And with the Iran struggle anticipated to extend the price of vitality, meals and gas, Greggs is unlikely to catch any respite.

And regardless of that, FTSE250 The corporate opened 121 web new shops final yr and plans to open an analogous variety of shops this yr, however traders worry it has reached “peak Greggs”. Can a model actually open greater than 3,000 places with out cannibalizing current retailer gross sales? It is clear the market is not satisfied.

Added to that is the rise of GLP-1 medication equivalent to; Munjaro The corporate has been pressured to alter its menu. Because of this, there are actually as many egg pots in Greggs’ fridges as there are sausage rolls behind glass counters.

The rising use of GLP-1 medication for weight reduction is altering dietary habits and decreasing the demand for high-calorie meals. We research these tendencies and innovate with merchandise that help satiety and balanced diet, together with fiber, plant-based and protein-rich merchandise..

Greggs 2025 Annual Report.

Are bakeries in peril of shedding their id because of the push in direction of more healthy meals? Sure.

In abstract, there are lots of components influencing inventory costs at the moment.

- Slower development.

- Earnings below strain.

- Rising UK unemployment price.

- Continued strain on residing prices.

- Peak Greggs Concern.

- Lower in foot site visitors on predominant streets.

- Potential affect on GLP-1.

A few of these components have made Greggs presently the subsequent most shorted inventory within the UK. evestock and Wizz Air. So refined traders predict extra ache to come back.

Not all the pieces is hopeless and gloomy

Regardless of the apparent challenges, Greggs nonetheless has many interesting qualities. The corporate has a singular model, a robust steadiness sheet, and (regardless of latest pressures) industry-leading revenue margins.

Moreover, it has a well-covered future dividend yield of 4.2%. That is above the FTSE250 common.

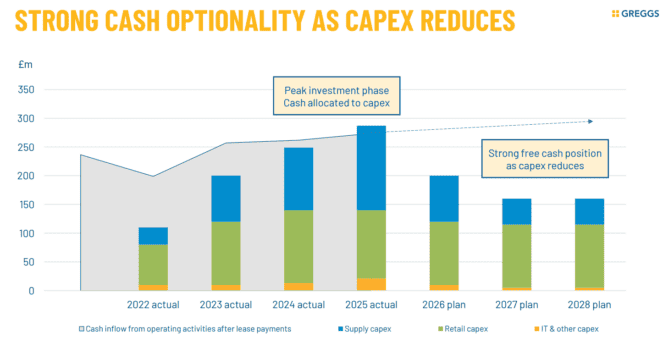

It is also value mentioning that capital spending peaked final yr, which ought to considerably enhance money move going ahead. Moreover, robotic order selecting at one in all two new state-of-the-art distribution facilities opening quickly ought to enhance effectivity.

One other factor I like is that about 20% of our shops are franchised (managed by third-party companions). These focus totally on roadside shops and due to this fact are likely to outperform company-operated shops. Each day operating prices (hire, electrical energy invoice, and so forth.) can even be collected.

Lastly, the inventory seems low-cost proper now. Primarily based on 2027 projections, the longer term price-to-earnings ratio is 12.5.

For affected person traders with a multi-year funding horizon, we predict this inventory is a shopping for alternative value contemplating now.