{kind=link}

Picture supply: Getty Photos

of FTSE100 Immediately (March twenty sixth) there weren’t many shares that had been up, because the inventory was down 1.3%. Because of this, Subsequent (LSE:NXT) stood out like a lighthouse after rising 5.2% to 12,665p.

This could come as a reduction to shareholders, because the inventory had fallen 12% year-to-date earlier than at this time’s surge. So what made at this time’s market joyful?

wonderful outcomes

Immediately’s rally was triggered by the clothes and residential items retailer’s annual outcomes for the monetary 12 months ending January 2026. As is commonly the case with Subsequent, it has damaged via the doom and gloom of Britain’s long-struggling retail trade.

Full-year gross sales rose 10.8% to £7bn, with development of seven% within the UK and 35% abroad. These numbers far exceeded the preliminary steerage (5% gross sales development) given practically a 12 months in the past.

In the meantime, pre-tax income rose 14.5% to £1.16bn, and earnings per share rose 17%. The enterprise generated free money movement of £1.1bn, which was uncommon. The corporate returned £839m to shareholders via dividends and share buybacks.

However whereas gross sales for the primary eight weeks of the 12 months had been promising, administration is turning into cautious because of the Center East wars. It expects full-year gross sales to rise by 4.5% and pre-tax revenue to rise by the identical quantity to £1.21bn.

However CEO Simon Wolfson warned that if the disruption lasts for greater than three months, Subsequent must elevate costs.1% to most 2%“However it may very well be much more relying on value inflation.

The danger going ahead is that customers fed up with inflation will shortly buckle up, hurting gross sales development.

Three issues

Is Subsequent a inventory price contemplating for long-term traders?To reply this, I believe there are three fundamental issues. These are the standard of the enterprise, future development alternatives, and valuation.

By way of high quality, I believe Subsequent ranks among the many finest. In September I referred to as it “cream of crop” amongst UK retailers, and final 12 months’s outcomes present why.

For example, contemplate the next quote from the report:Each exercise we undertake, from a brand new warehouse or advertising and marketing marketing campaign to the launch of a brand new model, have to be evaluated when it comes to profitability and return on funding. We don’t bask in initiatives that some might contemplate “strategic”, however with little expectation of excessive returns or wholesome income.”

After all, it sounds easy. However with world-class administration and execution, Subsequent does not simply discuss, it takes motion. Many retailers do not.

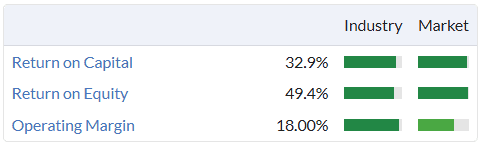

That is mirrored in our wonderful high quality indicators.

As for future development, I believe Subsequent has barely scratched the floor of its long-term worldwide alternatives. Worldwide on-line gross sales reached £1.3 billion final 12 months, which is a big drop for a worldwide market.

For instance, we purpose to broaden our gross sales in Asia and the US with much less capital via our on-line aggregator platform. And given the UK’s financial stagnation, this can develop into much more essential going ahead.

What about scores? Now, surprisingly, this blue-chip inventory just isn’t low cost, with a ahead P/E of round 16 occasions (above the 10-year common of 13.5 occasions).

Nonetheless, Subsequent has strict standards for share buybacks, that are presently set at £131. So, at a share worth of £126, I believe it is price contemplating, particularly throughout a Center East-related downturn.