{kind=link}

Picture supply: Getty Photographs

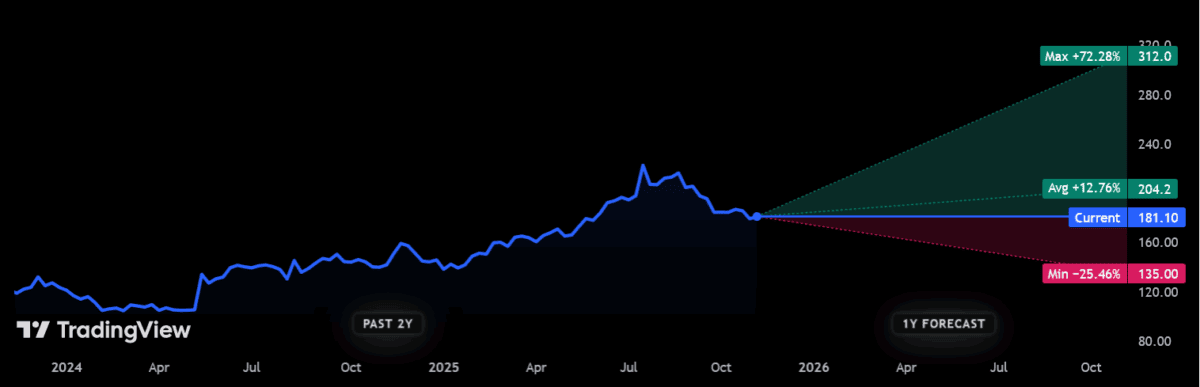

of BT (LSE:BT.A) inventory is up a formidable 23% year-to-date. And metropolis analysts do not assume so. FTSE100 Inventory continues to be operating out.

BT shares final traded at 181p per share. If predictions are right, the share worth will break above 200p over the subsequent 12 months, at 204.2p per share. This may be a 12% improve from present ranges.

Considering the forecast dividend, BT traders may probably understand a complete return of 16% to 17% over the subsequent 12 months. However how practical are these predictions?

progress

Firstly, you will need to notice that not all brokers make bullish estimates throughout the board. This 200p+ goal is the typical of 15 forecasts at the moment offered by the analyst group.

One analyst believes BT’s share worth may fall by greater than 1 / 4 between now and Memorial Day subsequent 12 months. That being mentioned, different estimates counsel costs may rise by greater than 70% in the course of the interval.

What do Citi analysts imagine can drive the corporate additional? Bulls imagine BT’s restructuring program is not going to solely assist it proceed its spectacular cost-cutting technique. They see this as a technique to rationalize their product vary and revive flagging earnings.

BT’s turnaround plan delivered vital financial savings value £1.2bn within the 18 months to September, exceeding expectations.

Optimism can be spreading to the corporate’s profitable Openreach infrastructure division as new fiber connections proceed to develop. We plan to attach 25 meters of plots by the tip of subsequent 12 months and 30 meters of plots by the tip of this decade.

Drawback

However whereas BT is making progress on these fronts, I am involved that the share worth goes nowhere as issues persist elsewhere.

The corporate nonetheless hasn’t proven how one can overcome its gross sales issues. Adjusted gross sales fell once more by 3% within the six months to September, with reversals recorded throughout the buyer, enterprise and worldwide sectors. With rising competitors and the UK’s financial downturn, it appears unlikely that the income downside can be resolved anytime quickly.

On the identical time, capital spending continued to rise, rising by 8% in six months. Which means that internet debt has additionally steadily elevated, rising by an additional 3% year-on-year to £20.9bn by the tip of September.

An much more sobering view is warranted when contemplating the price of BT’s large pension deficit. It will value the corporate round £800m a 12 months.

costly

There are additionally valuation points that we expect may restrict additional upside in BT’s share worth. Attributable to this 12 months’s surge, the ahead worth/earnings ratio (PER) is 10.3 occasions.

That is greater than the 10-year common of 8.8 occasions. This new premium is very obscure given the persistent challenges companies face.

Along with this, BT inventory has a price-to-book ratio (P/B) of 1.4x. That is up from under 1 simply 14 months in the past, indicating that the corporate is buying and selling at a premium to its asset worth.

I would not be stunned if BT’s share worth continues to rise. However I do not assume it stands an opportunity, so I would relatively purchase UK shares, that are a lot much less dangerous.